You can buy land, build a house to claim full exemption on total costs, including construction Selling long-term capital assets can yield a windfall but also attract hefty capital gains tax. If you plan to sell such assets, you can save tax under sections 54 and 54F of the Income Tax Act by reinvesting the proceeds in a house.

Section 54 applies when you sell a residential property. You can claim exemption on long-term capital gains (LTCG) by using the gains to buy another residential property. The new house must be bought within one year before or two years after the sale, or constructed within three years.

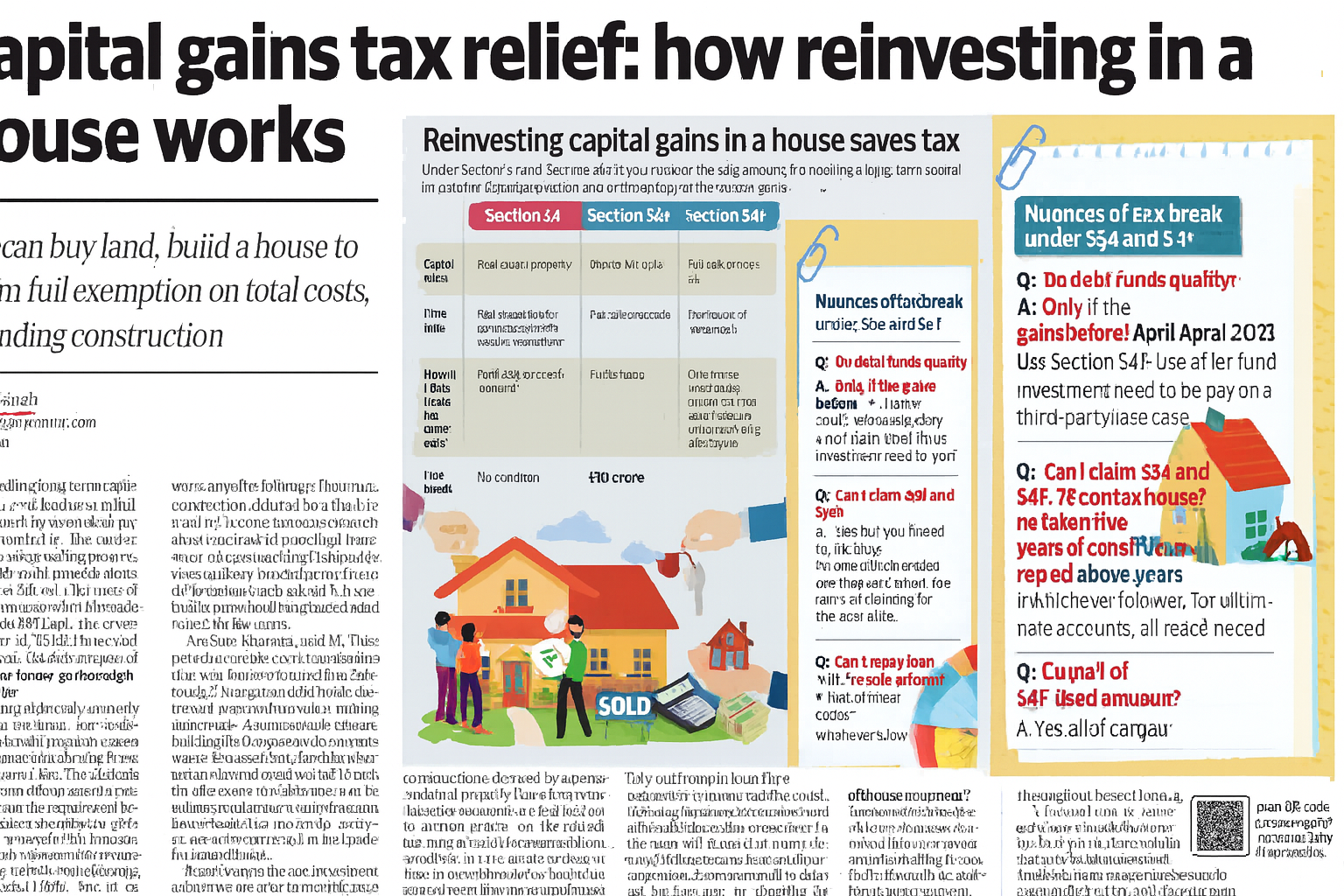

Section 54F extends this benefit to gains from other capital assets such as domestic and overseas shares, equity mutual funds, gold, or commercial property. But it comes with stricter rules: you must reinvest the full sale proceeds, not just the gains, and you cannot own more than one house at the time of sale. Under both sections, the exemption is withdrawn if the new house is sold within three years of purchase. There are other nuances too — in joint ownership, the exemption applies only to your share of the purchase or sale value. Mint explains how sections 54 and 54F work and how they can help reduce your tax burden.

Do gains from debt funds qualify for exemption?

No. Only long-term capital gains (LTCG) qualify for exemption under Section 54F. “Since the July 2024 budget changes, assets such as debt mutual funds, market-linked debentures and unlisted bonds are treated as short-term regardless of holding period. Hence, gains from these aren’t eligible for 54F exemption,” said Neeraj Agarwala, partner, Nangia & Co LLP.

However, debt funds bought before 1 April 2023 still qualify for LTCG exemption, said Parizad Sirwalla, partner and head, global mobility services, KPMG. Investments made before that date and redeemed after three years are treated as long-term. From 23 July 2024, the holding period for long-term gains was cut to two years, so debt fund units purchased before 1 April 2023 and sold after 23 July 2024 will qualify as long-term holdings.

Can I claim benefits under both sections on one property?

Yes, it is allowed if all qualifying conditions are met. Riaz Thingna, partner, Grant Thornton Bharat, said courts have time and again affirmed that these provisions are not mutually exclusive. “The key is that under Section 54 the exemption will be restricted to the amount of capital gain reinvested, and under 54F it will be proportionate to the net sale value reinvested. And the combined exemption cannot exceed the actual cost of the new property or Rs 10 crore, whichever is lower.”

For example, if you sell shares worth Rs 50 lakh (eligible under Section 54F) and a house with a gain of Rs 80 lakh (eligible under Section 54), and buy a new house for Rs 1 crore using Rs 50 lakh from each sale, you get an exemption on Rs 50 lakh from the house sale while the remaining Rs 30 lakh is taxed.

Is exemption allowed for under-construction properties delayed by over three years?

This is a grey area, but courts have allowed exemptions when delays are the builder’s fault, said Neetu Vinayek, partner and tax infrastructure leader, EY India. “It’s only allowed in cases of nominal delays or where the entire amount has been invested in a new residential property that has been substantially completed but not yet fit to be occupied. That said, in such cases the taxpayer has to demonstrate that the delay is beyond their control,” she said.

Thingna said: “In such cases courts allowed exemption only when the taxpayer gave bona fide explanation and evidence that the delay was due to the builder.”

I’ll pay the builder in instalments over two years and withdrew my MFs in one go. How do I claim the exemption?

In this case, the amount paid to the builder from your MF proceeds in the year of sale qualifies for exemption, said Vinayek. “The amount left must be deposited in the Capital Gains Account Scheme (CGAS) prior to filing the income tax return,” he added.

For instance, if you sold MFs worth Rs 1 crore in FY26 and used Rs 50 lakh to pay the first instalment, deposit the remaining Rs 50 lakh in a CGAS account before filing your FY26 return. You can withdraw it to pay subsequent instalments. This ensures exemption on Rs 1 crore and avoids tax at the time of filing.

The CGAS balance must be used for construction within three years of sale. Any amount left after that will be taxed.

Can I repay a home loan with sale proceeds and get an exemption?

Yes, if other conditions are met. “The object of beneficial provisions (sections 54 and 54F) is to help taxpayers invest in residential units. Hence, courts held there is no statutory mandate under Section 54 requiring the very same sale consideration to be used for acquiring/constructing a new residential house,” said Thingna. In other words, you can use sale proceeds to pay your outstanding home loan and get an exemption on this amount.

I bought a house for exemption benefits but want to gift it to my spouse or adult child. Will I lose the benefits?

Both sections 54/54F requires the new property to be held for three years. If transferred sold or earlier, the exemption is withdrawn. The tricky part is whether gifting counts as transfer. While gifts aren’t taxable as capital gains, 54F doesn’t explicitly exclude them, said Sirwalla. “Few court rulings allowed deduction, subject to certain conditions, but considering the conflicting rulings that are fact-specific, deductions may be challenged and eventually revoked.”

Agarwala said under Section 47, gifting isn’t treated as taxable transfer even though ownership changes. “A ‘transfer’ generally covers sale, exchange or transfer of possession for consideration. This doesn’t happen in gifting, so gifting a property to relatives must not, in principle, revoke the exemption.”

Still, this is a grey area. “Tax authorities scrutinised such transactions. Tribunals took fact-specific views, considering the intent of transfer,” Agarwala added. If gifting within three years, be prepared for possible litigation and ensure strong documentation of intent.

I spent Rs 40 lakh on a plot and plan Rs 60 lakh for construction. Will exemption apply to Rs 1 crore or only Rs 60 lakh?

Under Sections 54 and 54F, buying a vacant plot doesn’t qualify for exemption, but building a house on it does. “Tax department circulars and court rulings say the cost of land is treated as part of residential house cost, whether bought or constructed. So, if sale proceeds are used to buy a plot and build a house, the total cost can be claimed for deduction,” Sirwalla said.

But construction must be completed within three years, Agarwala added.