Fixed Income instruments are those instruments that provide a fixed rate of return at a specified time to the investors. These types of investments offer diversification to the investors as they are less risky than equities and other asset classes. These instruments best fit for the risk-averse investors who want safety and a fixed income.

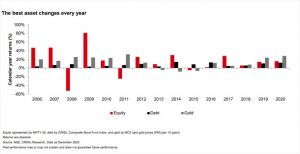

Let us take a look at a chart:

In the chart above, we can clearly see that equity and gold returns have been quite volatile, but debt has provided steady and consistent returns. Even though debt is providing less return as compared to equity, it is safe and provides a healthy return.

Some of the safest investment options available to an investor are:

1. Public Provident Fund (PPF)

PPF is believed to be amongst the safest fixed-income securities in India.

In 1968, the Ministry of Finance (MOF) introduced PPF to provide long-term retirement planning options to individuals:

- Who are not covered by provident funds of their employers, or

- To those who are self-employed.

- PPF is backed by the Government of India, which means PPF has a sovereign guarantee for the returns. Thus, PPF is a significant savings instrument.

- PPF is a tax-free instrument as you can get a deduction u/s 80C for the amount invested and interest earned on it.

- Any Indian citizen, except for an NRI, can open a PPF account. However, he/she can have only one account in his/her name.

- The minimum tenure for which a PPF account can be opened is 15 years. After that, you can extend that period in blocks of 5 years.

- Opening a PPF account is very easy and you just need Rs. 100 to open it. After that, they need to invest a minimum amount of Rs. 500 each year and the maximum amount of Rs. 1,50,000 each year.

- An individual can withdraw his balance from the PPF account only upon reaching maturity, i.e., after 15 years.

If an individual wants to withdraw money before that, he can do it after five years, but he will have to pay the penalty. - PPF offers a floating interest rate, i.e., interest rates change every quarter. The current interest rate is 7.10% p.a., compounded annually.

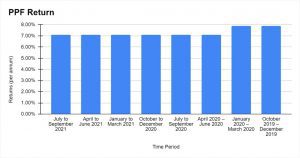

The historical return of PPF is as follows:

2. Bank Fixed Deposits (FDs)

The most favourite investment options for many Indians have been bank fixed deposits. A fixed deposit is a very safe instrument and, as the name suggests, offers a fixed rate of return.

A fixed deposit is an instrument where your money is deposited for a fixed period at a fixed interest rate. After the period ends, you will receive the amount you invested plus the interest earned over the period.

Almost all banks offer fixed deposits. Depending upon your period, you can select a fixed deposit. Usually, banks have fixed deposits ranging from 7 days to 10 years.

The interest rate on an FD is fixed when you open the account, and it depends on the tenure of your FD.

Thus, even if the interest rate in the market changes, FDs will give you the interest it has promised. Due to this reason, we can say FDs are very safe (as the principal amount is safe) and offer guaranteed returns.

However, there is one disadvantage of holding a Bank FD. You will not be able to withdraw money before maturity; a penalty is charged from you if you do so.

The current interest rates offered by different banks are:

| Name of Bank | For General Citizens (p.a.) | For Senior Citizens (p.a) | Tenure Period |

| State Bank of India FD | 2.90% to 5.40% | 3.40% to 6.20% | 7 Days to 10 Years |

| HDFC Bank FD | 2.50% to 5.50% | 3.00% to 6.25% | 7 Days to 10 Years |

| Punjab National Bank FD | 2.90% to 5.25% | 3.50% to 5.75% | 7 Days to 10 Years |

| Canara Bank FD | 2.90% to 5.25% | 2.90% to 5.75% | 7 Days to 10 Years |

| Axis Bank FD | 2.50% to 5.75% | 2.50% to 6.50% | 7 Days to 10 Years |

3. Government T-bills/Bonds

If you require money, you will go to a bank. Similarly, if the government needs money to build dams, hospitals, roads, etc., it will go to the RBI, who will then auction the loan in the form of T-bills/bonds.

T-Bills (Treasury bills) are government securities that have a maturity of less than 1 year, and bonds are securities that have a maturity of greater than 1 year. These instruments are risk-free as the government backs them.

The maturity of the Government bonds ranges from a few months to many years.

The Government can offer both a fixed and a floating rate bond. The government, just like any borrower, will pay the principal amount and the remaining interest at the end of the maturity period. You can also sell the bond before maturity.

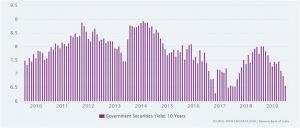

Currently, the 10 year Government Bond has a yield of 6.639%.

The historical return offered by Government Securities is as follows:

4. National Pension Scheme (NPS)

The NPS was launched in 2004 by the Government of India to provide a regular income to Indian citizens after their retirement.

It is a voluntary retirement savings scheme sponsored by the Government that helps individuals to make defined contributions, thus safeguarding their future by receiving a pension.

The rules and regulations for the NPS scheme are formed by the Pension Funds Regulatory and Development Authority (PFRDA).

Any citizen of India, who is between 18-65 years, whether resident or non-resident can open NPS.

After retirement, the account holders of NPS can withdraw a certain percentage of their corpus, and after that, they will receive the remaining amount as a monthly pension.

Usually, NPS provides returns that are higher than other instruments like PPF. NPS also offers tax benefits to investors.

The returns on an NPS investment depend upon the performance of the underlying assets. However, they have generally provided a return of over 9%-11% over 10 years.

5. National Savings Certificates (NSC)

NSC is a fixed income instrument that carries a very low risk and provides fixed income.

If you want to open an NSC, you can visit any post office branch. However, NSC has a lock-in period of 5 years. In an NSC, you should make a minimum investment of Rs. 1000. If an individual invests in NSC, he/she will also get an exemption of up to Rs. 1.5 lakh per annum u/s 80C.Currently, the interest rate on NSC is 6.8% p.a. The Government revises the interest rate every quarter.

6. Corporate FDs

Just like bank FDs, an individual can also invest in corporate FDs. The only difference is that the FDs are offered by corporates and NBFCs rather than banks.

It is a term deposit where you invest your money for a fixed period at fixed rates of interest.

Different banks offer different maturities corporate FDs ranging from a few months to a few years.

Generally, if you invest in a corporate FD, you will get a higher interest rate than a bank FD. Not only this but Corporate FDs are also considered to be more liquid as they have a lower lock-in period.

However, Corporate FDs are not as secure as Bank FDs.

The current Corporate FD Interest Rates are as follows:

| Company Name | Interest Rates (p.a.) | ||

| 1-year | 3-year | 5-year | |

| Shriram Transport Finance Co. Ltd. | 6.31% | 7.25% | 7.48% |

| Shriram City Union Finance Co. Ltd. | 6.31% | 7.25% | 7.48% |

| Kerala Transport Development Finance Corporation Ltd. | 6.00% | 6.00% | 5.75% |

| PNB Housing Finance Ltd. | 5.90% | 6.60% | 6.70% |

| Sundaram Home Finance | 5.50% | 5.80% | 5.80% |

7. Corporate Bonds

Companies also require money for various reasons such as expansion, buying new equipment, etc. So, they issue bonds to raise money, which is known as corporate bonds.

These bonds generally come with medium to long-term maturity. Both private and public companies can issue corporate bonds. Corporate bonds come with different credit ratings.

Just like government bonds, these bonds also provide regular interest at a predefined time, and after maturity, the principal amount is also given back.

Corporate bonds often provide higher interest rates as compared to government bonds. So, it can be said that corporate bonds are a good option for investors who want fixed higher income and for those who are looking for safety as corporate bonds are considered to be safer than equity.

The current interest rate on some corporate bonds is:

- Canara Bank – 9.55%

- Shriram Transport Finance Company Limited – 10.25%

- IDBI Bank Limited – 9.50%

Source: https://www.bseindia.com/markets/debt/tradereport.aspx

If you want to know more about corporate bonds, how they work, where you can buy from, how much interest you can earn, etc., you can contact a reputed wealth management advisory firm like RURASH.

Conclusion

Investing money wisely is very important. If you are an investor who is looking for a fixed income, then you have many options, few of which are mentioned above. Before selecting an instrument, you must be very clear about your financial goals, risk appetite, the period for which you want to invest, etc.

Before investing in an instrument, an individual should also understand the risks involved in it. Thus, make a choice that will best suit your needs.

RURASH is amongst India’s tech driven investment management company, providing financial solutions to augment the client’s wealth and facilitate building a legacy.

For any guidance regarding financial instruments, please reach out to us at invest@rurashfin.com or call us at +91 9820038401.

Also Read: Pillar of Indian Economy – 10 Indian blue chip companies.