The market regulator has suggested capping brokerage and transaction costs that mutual funds can charge investors. Fund houses are unhappy and their shares fell as much as 8% on Wednesday. Mint breaks down what this means for mutual funds and retail investors: What changes has Sebi proposed?

The Securities and Exchange Board of India (Sebi) has proposed capping the brokerage and transaction costs that asset management companies (AMCs) can charge investors over and above the total expense ratio (TER). This ratio is the annual cost that a mutual fund charges its investors. Since TER covers fund management, research, and operational expenses, Sebi aims to prevent investors from being charged twice for it. Sebi recommends reducing brokerage limits from 0.12% (12 bps) to 0.02% (2 bps) for cash market transactions and from 0.05% (5 bps) to 0.01% (1 bp) for derivatives. How will the capped charges affect MFs?

If implemented, AMCs will have to pay for research expenses instead of passing them on to investors. This means AMCs’ operating costs could rise, reducing profit margins in the short term. “The worst nightmare of any Indian institutional equities chief executive officer just came to life,” analysts at Bernstein said in a note. Institutional equity platforms that earn revenue from trade execution and research services may see lower overall income since AMCs might cut back on paid research. But the change would improve transparency by ensuring investors are charged for genuine execution costs, not bundled research fees. What can investors look forward to?

Sebi has recommended that mutual funds disclose upfront the all-inclusive TER with a clear breakdown of each component. It will improve transparency and allow retail investors to better understand what they pay for. A cap on additional charges may potentially boost returns for investors, say some market participants. But that may not be visible in the short term. What can be expected next?

Market participants expect AMCs to push back against Sebi’s proposals since they can eat into their profit. This affects asset managers, distributors and transfer agents. If Sebi decides to address the concerns raised, a round of discussions about how to manage any potential impact can be expected. If the AMC’s demands go unheard, they might pass on the cuts to distributors or brokers. The value chain will get affected and entities such as brokers and distributors will have to share the pain and costs, experts say. Will AMCs gain anything from this?

Sebi has recommended allowing AMCs to distribute investment management and advisory services to non-pooled funds for large, non-retail investors like family offices, pension funds or insurers. In such funds, each client’s money is kept separate and managed individually based on objectives, risk profile or mandate. AMCs will have to set up a separate business unit for it to ensure there is no information sharing. The move is perceived positively. Globally, AMCs are allowed to act as distributors and advisors.

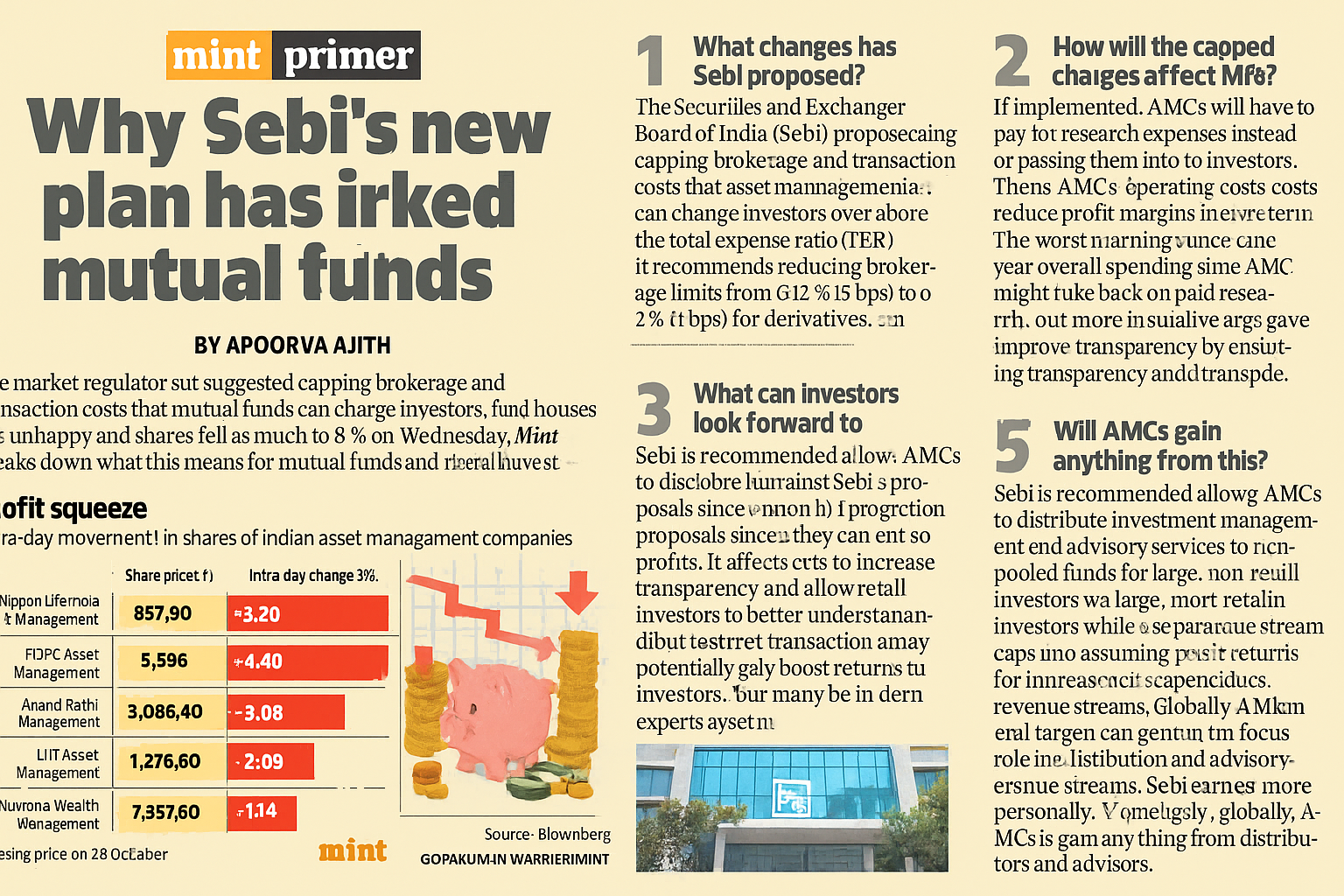

Nippon Life India Asset Management HDFC Asset Management Anand Rathi Wealth UTI Asset Management Nuvama Wealth Management

Nippon Life India Asset Management HDFC Asset Management Anand Rathi Wealth UTI Asset Management Nuvama Wealth Management