The 50/30/20 rule is a popular budgeting method designed to help individuals manage their income effectively while maintaining a balance between present needs and future financial security. It divides after-tax income into three clear categories, making financial planning easier and more structured.

What is the 50/30/20 Rule?

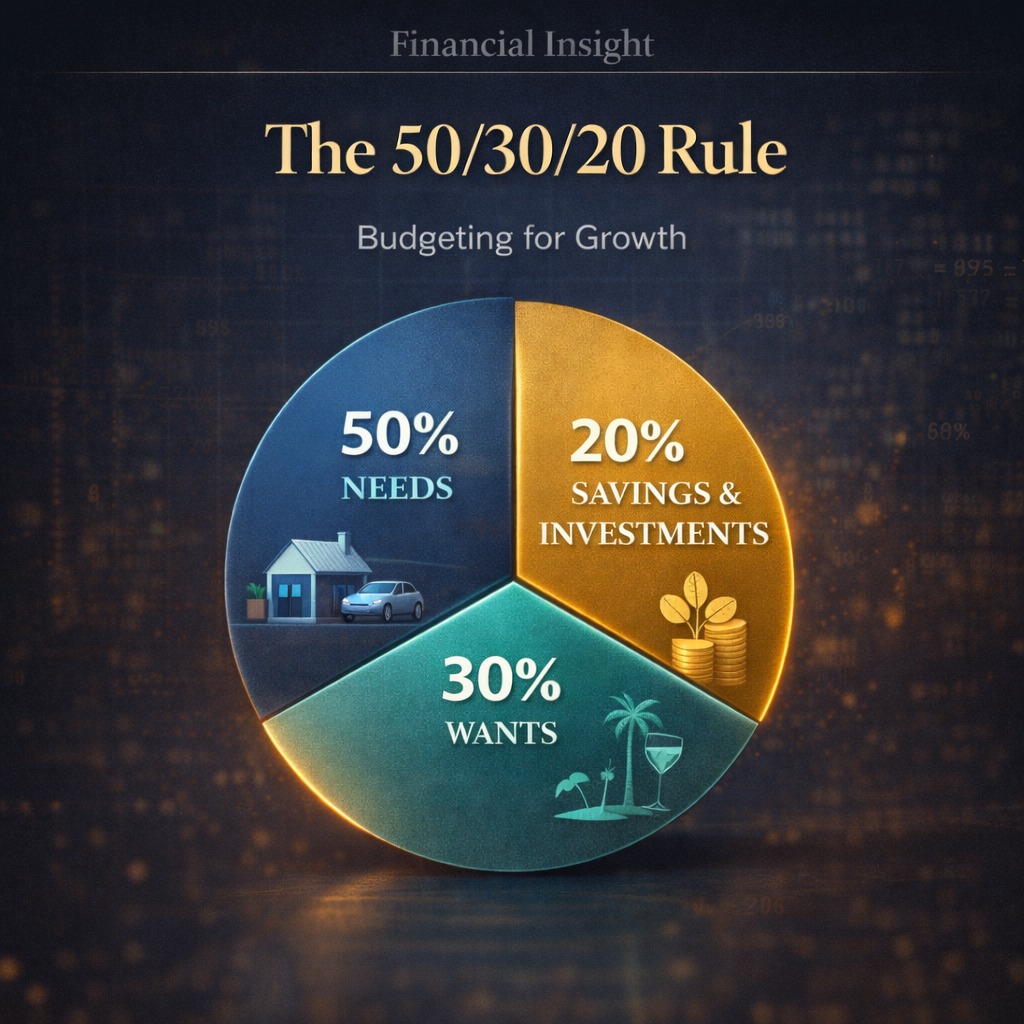

The rule suggests allocating your income as follows:

50% for Needs

30% for Wants

20% for Savings and Investments

This structure helps ensure that essential expenses are covered, lifestyle choices remain affordable, and long-term financial goals are not neglected.

1. The 50% – Needs

Needs are unavoidable expenses required to maintain your basic standard of living.

These typically include:

• Housing (rent or home loan EMI)

• Utilities such as electricity and water

• Groceries

• Insurance premiums

• Transportation

• Minimum loan repayments

• Essential healthcare

If your needs exceed 50%, it may indicate that fixed expenses are too high relative to

income, potentially limiting your ability to save.

2. The 30% – Wants

Wants represent discretionary spending — things that improve comfort and lifestyle but are not strictly necessary. Examples include:

• Dining out

• Travel and vacations

• Entertainment subscriptions

• Shopping beyond essentials

• Gadgets and upgrades

• Hobbies

This category ensures that financial discipline does not come at the cost of enjoying the

present. A sustainable plan allows room for both responsibility and lifestyle

satisfaction.

3. The 20% – Savings and Investments

This portion is directed toward future financial strength. It may include:

• Retirement savings

• Equity or debt investments

• Emergency fund contributions

• Children’s education planning

• Prepayment of loans

• Long-term wealth creation strategies

Consistently allocating 20% toward this bucket can significantly improve financial

resilience and help build long-term assets through compounding.

Why the 50/30/20 Rule Matters

The strength of this framework lies in its simplicity. Instead of tracking dozens of

spending categories, individuals can focus on maintaining proportional balance.

It encourages:

• Financial discipline without excessive restriction

• Regular saving habits

• Conscious spending

• Reduced financial stress

• Greater preparedness for unexpected events

Most importantly, it promotes the habit of paying yourself first — prioritizing savings

before discretionary spending expands.

Is the Rule Fixed for Everyone?

The 50/30/20 rule should be viewed as a guideline rather than a rigid formula. Financial

situations vary depending on income level, city of residence, family responsibilities, and

life stage.

For example:

• Early-career professionals may initially spend more on needs due to housing

costs.

• Higher earners may choose to increase the savings percentage.

• Individuals nearing retirement often prioritize savings beyond 20%.

The objective is not perfect adherence but maintaining a thoughtful allocation that

supports both present stability and future growth.

The Deeper Insight Behind the Rule

At its core, the 50/30/20 approach is about intentional financial behavior. Without a

framework, spending can gradually expand to consume income, leaving little room for

wealth creation.

By defining boundaries for needs, wants, and savings, individuals gain clarity over their

financial direction and reduce the likelihood of living paycheck to paycheck.

Over time, disciplined allocation can transform income into lasting financial security.

Conclusion

The 50/30/20 rule offers a practical starting point for anyone seeking structure in

personal finance. It recognizes that a healthy financial life is not solely about saving

aggressively or spending freely, but about maintaining equilibrium between the two.

When applied consistently, this method supports both immediate lifestyle needs and

long-term financial aspirations, laying the foundation for sustainable growth and

stability.