Smart Ways to Reduce LTCG Tax on Equity: A Practical Guide for Investors

Long‑term capital gains (LTCG) on listed shares and equity mutual funds have become a natural part of most retail investors’ wealth‑building journey. But a growing portfolio does not have to mean a growing tax burden.

With smart planning—using available exemptions, optimizing timing, and structuring family holdings efficiently—investors can significantly improve their post‑tax outcomes while staying fully compliant with the Income Tax Act, 1961.

1. Using Section 54F: The Most Powerful LTCG Exemption Tool

One of the most effective ways to reduce LTCG tax from equity is reinvestment via Section 54F, available to individuals and HUFs.

Eligibility

You can claim exemption on LTCG from equity if the net sale consideration is invested in one residential house in India.

Timelines to Follow

Purchase a residential property

• Within 1 year before or

• Within 2 years after the saleConstruct a residential property

• Within 3 years of saleIf you cannot invest immediately, deposit the amount in a Capital Gains Account Scheme (CGAS) before the tax‑return due date to retain eligibility.

When the Exemption Can Be Withdrawn

The benefit is revoked if:

The new house is sold within the lock‑in period

Funds are not utilised within the statutory window

You own more than the permitted number of residential houses on the date of transfer

CGAS deposits are not used correctly

Note: The earlier option of Sec 54EC bonds cannot be used for equity gains anymore—making 54F the primary mechanism.

2. Tax-Loss Harvesting: A Smart Year-End Strategy

Effective tax planning also includes active portfolio management:

Set-off Rules

Short-term capital loss (STCL) → can be set off against both STCG and LTCG

Long-term capital loss (LTCL) → can be set off only against LTCG

Unused losses can be carried forward for 8 years if the tax return is filed on time.

Selling underperforming assets to realize losses can significantly lower your tax bill.

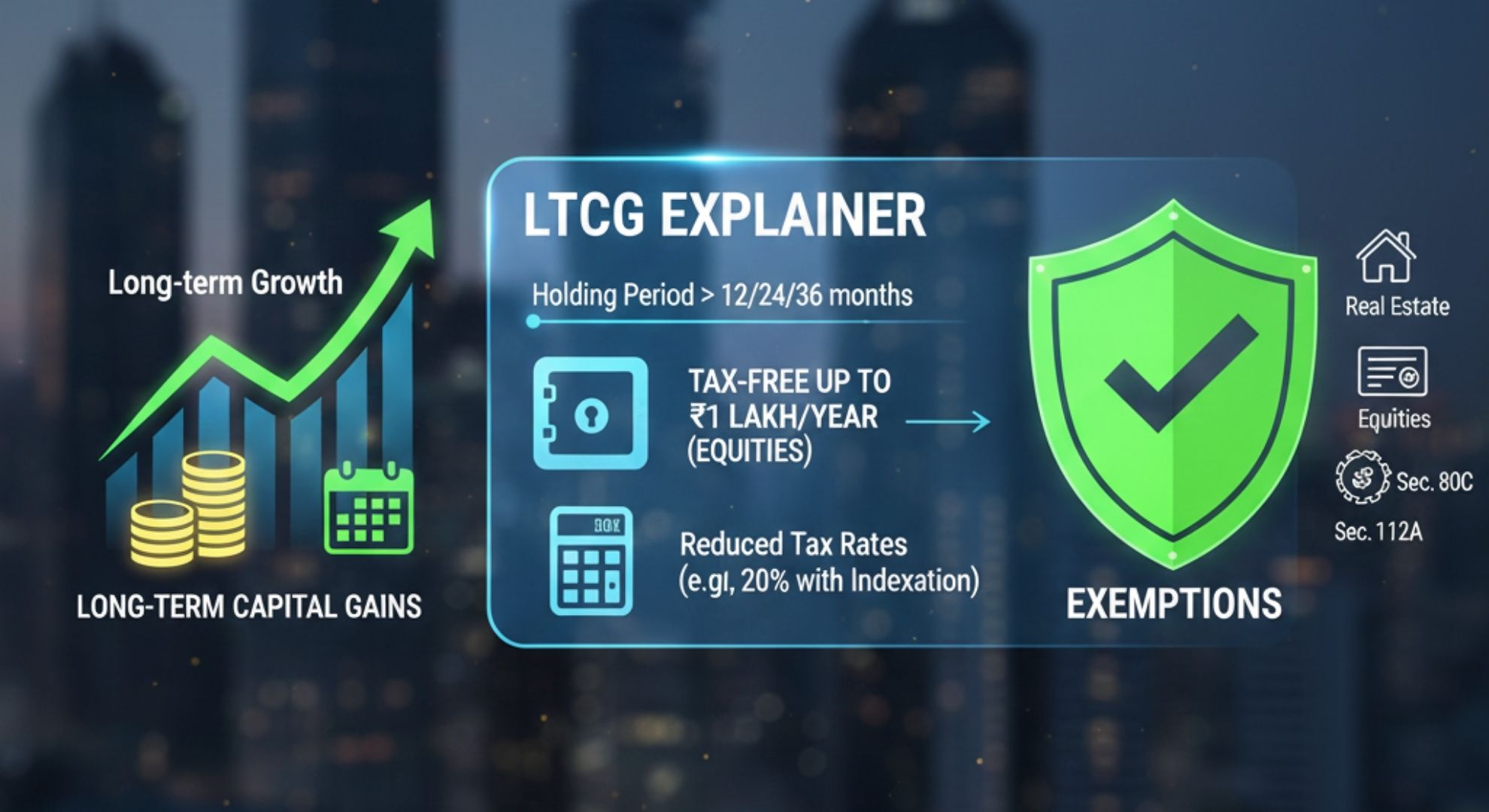

3. Making the Most of Section 112A Annual Exemption

LTCG on listed equity and equity mutual funds is taxed at:

12.5% + surcharge + cess

Applicable on gains exceeding ₹1.25 lakh per financial year.

You can reduce your tax outgo by:

Spreading profit‑booking across financial years

Ensuring you cross the 12‑month holding period to classify gains as long‑term

Monitoring gains throughout the year to optimise use of the ₹1.25‑lakh annual exemption

4. Using Family Structuring & Gifts—Legally and Safely

Gifting can also help reduce tax if executed correctly.

Tax-Free Gifts

Transfers of shares/units to specified relatives are tax‑neutral.

The recipient pays tax on future gains—subject to clubbing rules for minors and spouses.

Best Practices

Maintain separate demat accounts

Create clear gift deeds

Keep transparent documentation

This ensures clean ownership trails and avoids tax disputes.

5. Strict Documentation & Timelines Are Crucial

To avoid losing exemptions:

Complete Section 54F reinvestments within deadlines

Deposit unused funds in CGAS before return filing

Keep proper records for gifts, acquisition costs and holding periods

A small delay or oversight can jeopardize the entire tax benefit.

Conclusion

LTCG from equity need not feel like an unavoidable tax burden.

With disciplined planning—using Sec 54F, loss harvesting, annual exemptions, and family‑level structuring—investors can legally and efficiently optimize taxes while building long-term wealth.

Explore More Insights

For a deeper understanding of how wealth management, advisory excellence, and capital‑market strategies shape India’s financial ecosystem, explore guidance from Ranjit Jha (CEO)—a pioneer in research‑driven wealth advisory.

To learn how Rurash Financials empowers investors through:

AIF access

Portfolio engineering

Unlisted equity opportunities

Personalised wealth strategies