A Forward-Looking Approach: Rate Cut Expected as Softer H2 GDP Meets Record-Low Inflation

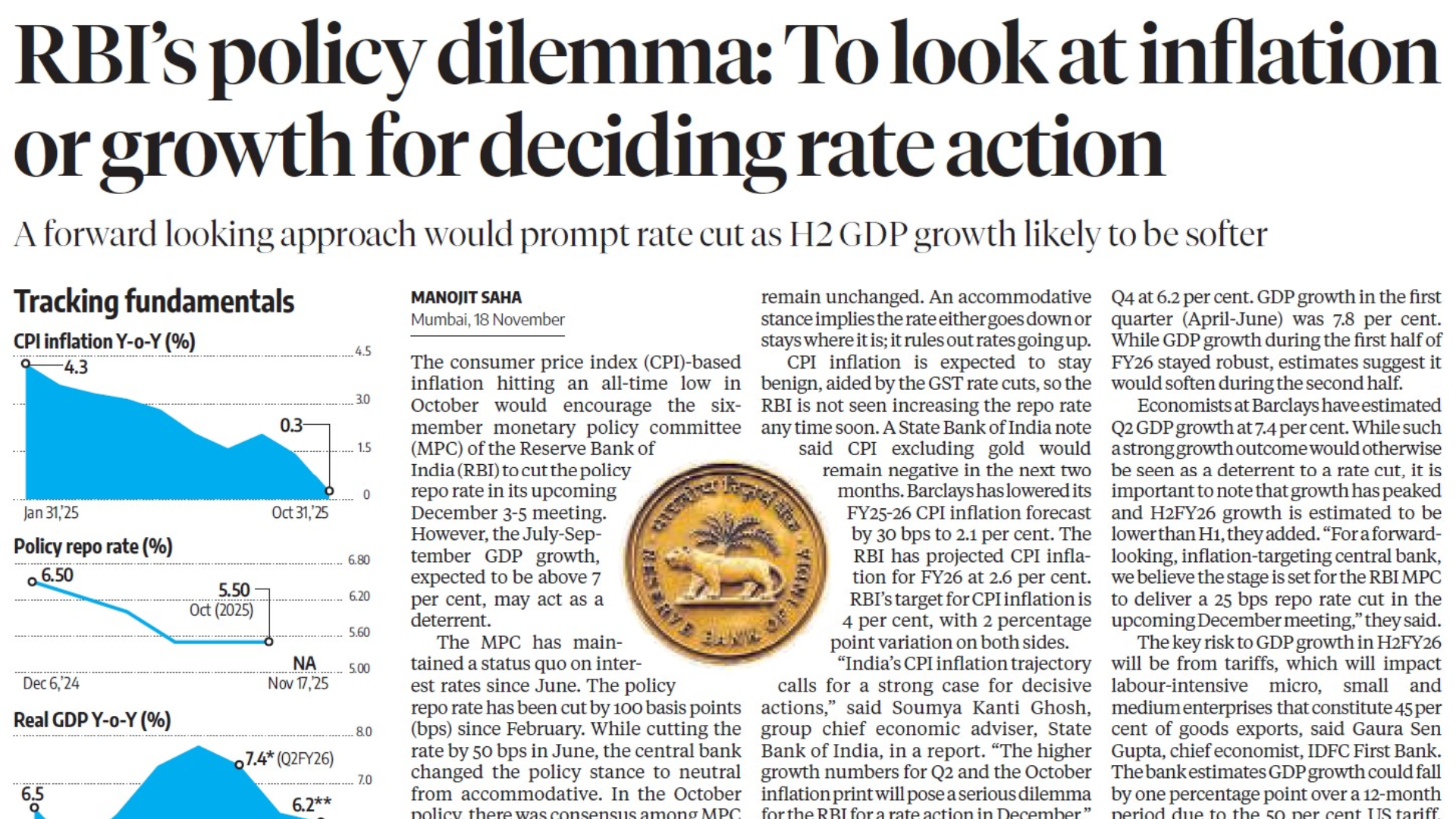

The stage is set for a pivotal monetary policy committee (MPC) meeting by the Reserve Bank of India (RBI) from December 3 to 5. 3 to 5. With the consumer price index (CPI)-based inflation hitting an all-time low in October, the six-member MPC is strongly encouraged to consider a policy repo rate cut. However, the robust July–September GDP growth, expected to be above 7 percent,percent, presents a complexity that the central bank must navigate.

The Inflation Argument: A Strong Case for Decisive Action

The MPC has maintained a status quo on interest rates since June, following a total reduction of 100 basis points (bps) since February. A key shift occurred in June when the central bank moved the policy stance from accommodative to neutral.

A neutral stance means the repo rate could go either up or down ordown or remain unchanged.

An accommodative stance implies the rate either goes down or stays put, ruling out rate increases.

With CPI inflation expected to remain benign, aided by recent GST rate cuts, the RBI is not seen increasing the repo rate any time soon

A State Bank ofIndia note projects that CPI excluding gold would remain negative in the next two months.

Barclays has lowered its FY25-26 CPI inflation forecast by 30 bps to 2.1 percent,percent, significantly below the RBI’s $\mathbf{4\% \pm 2\%}$ target band. The RBI’s own projection for FY26 is 2.6 percent.percent.

“India’s CPI inflation trajectory calls for a strong case for decisive actions,” .

The Growth Outlook: Peaking and Softening Ahead

While the low inflation print favors easing, the strong GDP growth figures pose a “serious dilemma” for the RBI. The central bank projected GDP growth for 2025-26 at 6.8 percent, with Q1 already at 7.8 percent.

Despite this, economists are focusing on the future trend:

| Quarter | RBI Projection | Growth Outlook |

| Q1 (Apr-Jun) | 7.8% (Actual) | Robust start to the fiscal year. |

| Q2 (Jul-Sep) | 7.0% | Barclays estimates this quarter at 7.4 percent. |

| Q3 (Oct-Dec) | 6.4% | Expected slowdown. |

| Q4 (Jan-Mar) | 6.2% | Expected slowdown. |

Economists at Barclays note that while strong Q2 growth would normally deter a rate cut, it is important to recognize that growth has peaked. Estimates suggest H2 FY26 growth is likely to be lower than H1.

“For a forward-looking, inflation-targeting central bank, we believe the stage is set for the RBI MPC to deliver a 25 bps repo rate cut in the upcoming December meeting,” they concluded.

Key Risks and Policy Constraints

The primary risk to the softer H2 GDP growth comes from tariffs, particularly impacting labor-intensive micro, small, and medium enterprises (MSMEs), which constitute 45 percent of goods exports.

Gaura Sen Gupta, chief economist at IDFC First Bank, estimates that a 50 percent US tariff could cause GDP growth to fall by one percentage point over a 12-month period.

The bank further cautioned, “Monetary policy space for rate cuts is limited; easing will depend on material downside risks to growth or a failure of the consumption recovery to sustain beyond the festival season.”

🔍 Explore More Insights

For a deeper understanding of monetary policy, macro trends, and interest-rate projections, explore perspectives from Ranjit Jha (CEO)—known for research-driven, long-term financial analysis.

To explore how Rurash Financials supports investors with fixed-income strategies, market research, and wealth solutions, visit the official website.