India’s leading non-banking financial companies (NBFCs) have said that allowing well-governed, upper-layer NBFCs to accept public deposits would help diversify their funding base, and reduce dependence on banks at a time when regulatory oversight and funding constraints are tightening.

In a panel discussion moderated by Manojit Saha of Business Standard, Rajiv Sabharwal, managing director and chief executive oicer (MD & CEO) of Tata Capital, emphasised that diversification of liabilities is now critical for the stability and competitiveness of NBFCs. “A good portion of our liabilities does come from banks. But a large opportunity has opened up in bonds, dollar bonds, and ECBs (external commercial borrowings) that’s now over 10 per cent of our liabilities. Public deposits would be another low-cost, stable source that helps reduce the linkage to bank funding,” he said. Sabharwal said that while the Reserve Bank of India (RBI) has in recent years encouraged NBFCs to reduce reliance on bank borrowings, access to public deposits has remained frozen for nearly two decades now. “It has been 15- 20 years since any new NBFC has received a deposit-taking licence,” he said. “If a start can be made, especially with upper-layer NBFCs and some thresholds in place, it would be a welcome step. Given the rising credit demand in the country, such access would amplify credit flow and support growth,” Sabharwal added.

The heads of NBFCs said that expanding the liability profile would be beneficial for the broader ecosystem. Sudipta Roy, MD & CEO of L&T Finance, said: “Access to public deposits will give us a low-cost deposit source, and will be very welcome if the RBI considers that for the upper-layer NBFCs.” The call for renewed access to public deposits comes amid a funding squeeze that followed the RBI’s decision to raise risk weights on banks’ lending to NBFCs. Industry leaders argue that a broader liability mix, including retail deposits, would enhance resilience and lower systemic concentration risks. Umesh Revankar, executive vicechairman at Shriram Finance, added that regulatory distinctions between banks and NBFCs have narrowed considerably in recent years. “It is no longer appropriate to think of the two sectors as one being regulatorily light and the other being more intensive. They are just two different business models that work for different kinds of players,” he said. With India’s credit demand rising sharply amid an expanding economy, the push for renewed deposit-taking rights highlights the sector’s ongoing efforts to secure stable, low-cost funding — and the RBI’s balancing act between financial inclusion, competition, and systemic prudence. Apart from accepting public deposits, there is no incentive to turn into banks, said the industry players. Jairam Sridharan, MD & CEO, Piramal Finance, said that the balance between banks and NBFCs in India has remained largely unchanged for decades now.

“If you look at the lending market 30 years ago and now, nonbanks have always been about a quarter of the lending sector,” he said. “There’s no particular reason for this to change. NBFCs have a distinct role — they are the last-mile connectors, more eicient in reaching customers banks often can’t. And their profitability has consistently been higher than that of banks,” Sridharan added. He further said that given this strong positioning, there’s “no burning platform reason” for NBFCs to become banks. “The only major differentiator is the ability to raise customer deposits. Apart from that, the pain of conversion outweighs the benefits,” he added. Sabharwal of Tata Capital also emphasised that both banks and NBFCs now operate under similar levels of governance and regulatory oversight. “Both models are strong. Both have delivered. It finally boils down to governance if that is strong, entities thrive. On governance, provisioning, and risk management, upper-layer NBFCs are comparable to banks. There’s nothing today that NBFCs can’t do,” he said. Revankar said that the primary motivation for NBFCs to convert into banks access to stable liabilities has diminished over time. “Fifteen years ago, NBFCs had limited liability options. But today, the capital markets are deep, ECB markets are open, and co-lending with banks has expanded. The liability side is no longer a constraint,” Revankar added.

He further said that NBFCs continue to fill critical gaps in financial inclusion. “NBFCs focus on the underbanked customers and segments banks find hard to serve. Banks expect customers to come to them; NBFCs go to customers. That agility and customer knowledge give us an edge,” he said, adding that NBFCs are growing faster than banks, with credit disbursement rising over 20 per cent compared with banks’ 10-12 per cent. “Even the finance minister recently said NBFCs could account for up to 50 per cent of total credit,” Revankar pointed out. Highlighting that many products were pioneered by shadow banks that was followed by commercial lenders, Raul Rebello, MD & CEO of Mahindra Finance, said: “While there were specific playbook for banks and NBFCs. That arbitrage is no longer available. NBFCs started vehicle lending, microfinance, gold lending- banks have actually picked up some good properties of NBFCs. .. In a country that is largely unnerved, the headroom for penetration is large.”

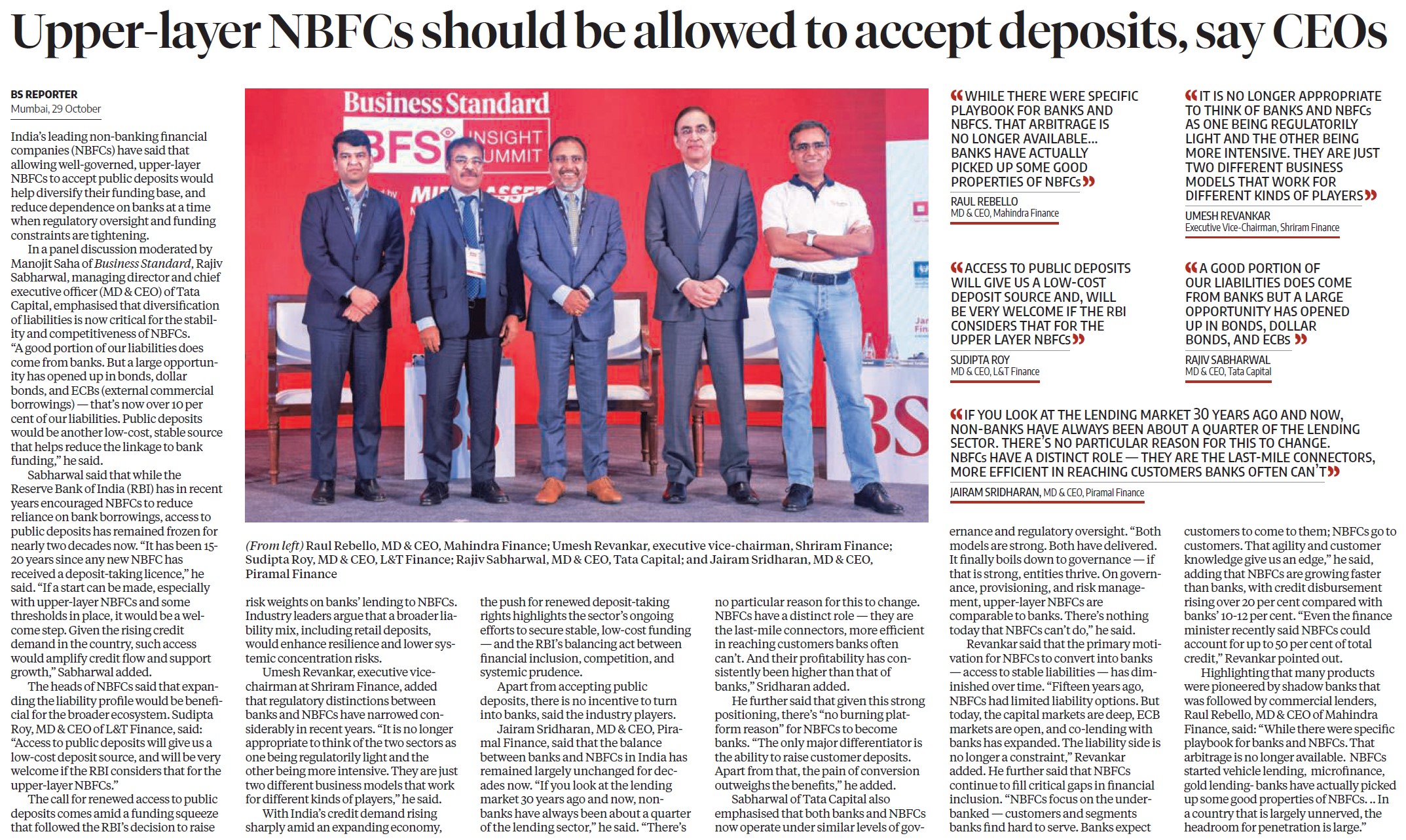

While there were specific playbook for banks and NBFCs. that arbitrage is no longer available… banks have actually picked up some good properties of NBFCs) RAUL REBELLO MD & CEO, Mahindra Finance

It is no longer appropriate to think of banks and NBFCs as one being regulatorily light and the other being more intensive. they are just two different business models that work for different kinds of players) UMESH REVANKAR Executive Vice-Chairman, Shriram Finance

Access to public deposits will give us a low-cost deposit source and, will be very welcome if the RBI considers that for the upper layer NBFCs) SUDIPTA ROY MD & CEO, L&T Finance

A good portion of our liabilities does come from banks but a large opportunity has opened up in bonds, dollar bonds, and ECBs ) RAJIV SABHARWAL MD & CEO, Tata Capital

If you look at the lending market 30 years ago and now, non-banks have always been about a quarter of the lending sector. there’s no particular reason for this to change. NBFCs have a distinct role they are the last-mile connectors, more efficient in reaching customers banks often can’t) JAIRAM SRIDHARAN, MD & CEO, Piramal Finance