Sebi Survey: Awareness of Investments Rises, But India’s Risk Aversion Persists

On the surface, a recent survey by the Securities and Exchange Board of India (Sebi) paints a promising picture of financial awareness across the country. In 2025, 53 percent of respondents—urban and rural combined—said they were aware of at least one securities-market product, such as mutual funds (MFs), even if they hadn’t invested.

A decade ago, in a comparable study, only 28.4 percent of urban respondents were aware of mutual funds. If rural India were included, the number would have been far lower. Clearly, awareness has grown—but awareness hasn’t yet translated into participation. Only 9.5 percent of Indians invest in securities-market products.

A Snapshot of Financial Awareness

The 2025 Sebi survey, which covered 53,000 respondents across urban and rural India, found:

53% of respondents were aware of at least one securities product.

Awareness was higher in urban areas (74%) versus rural (56%).

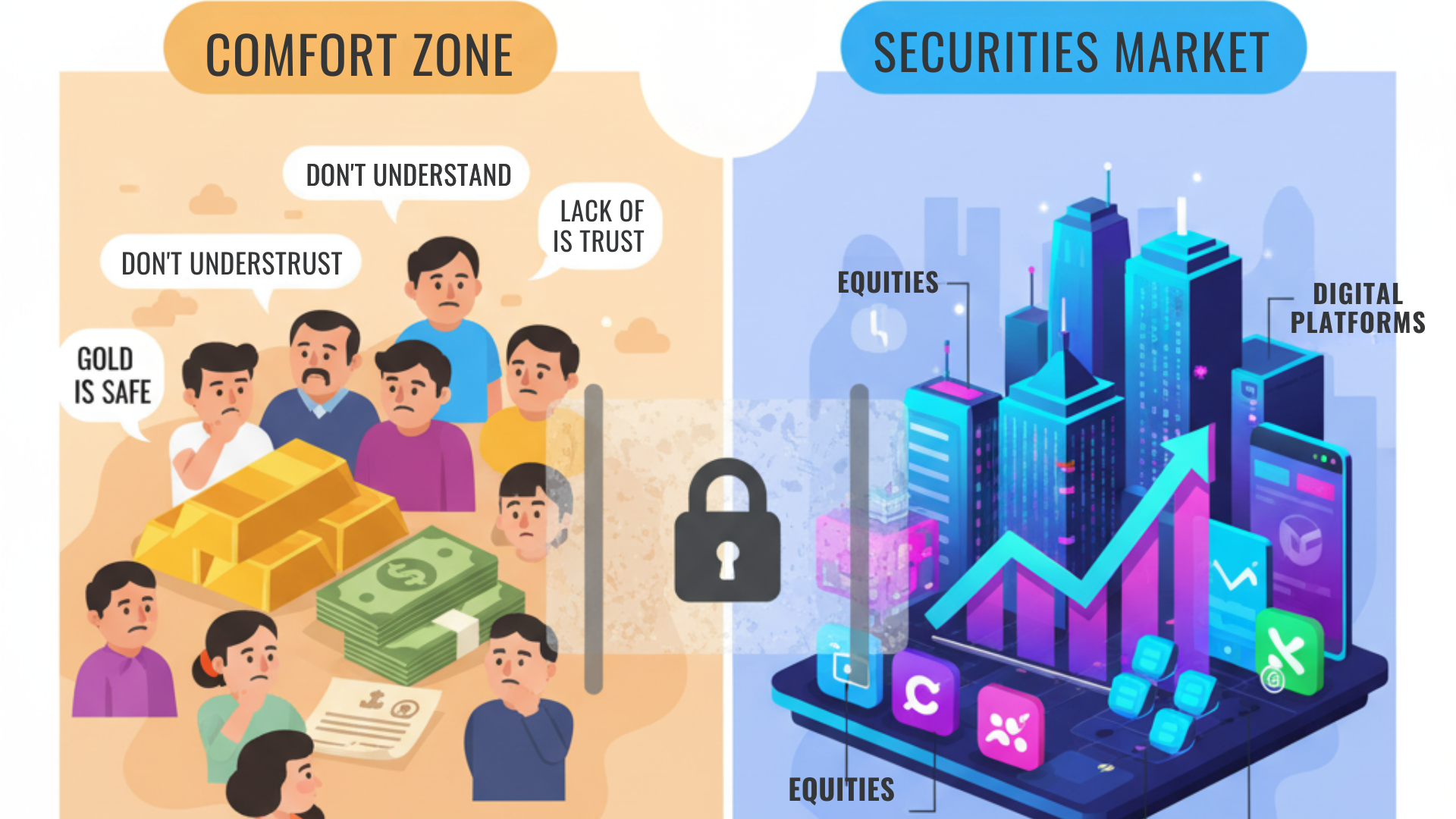

Mutual funds (53%) and equities (49%) topped the list, while awareness of more complex instruments such as futures, options, and REITs stayed below 13%.

While this marks progress, Sebi observed that penetration remains weak. Only 6.7% of respondents invest in MFs and 5.3% in equities—numbers that remain far below those of advanced economies.

Penetration Gaps and Demographic Divide

Investment penetration—defined as holding at least one market product—was 23% in the top nine metros, versus just 6% in rural India. Education levels significantly influenced participation:

27% of postgraduates had invested in at least one securities product.

19% of graduates reported similar engagement.

Even among investors, only three-fifths are active participants, highlighting limited ongoing engagement with financial markets.

High Awareness, Low Participation: The Risk Factor

The core challenge remains risk aversion. Despite greater access to information, 80% of respondents displayed low risk tolerance. Many equate “risk” with danger (33%), loss (23%), or uncertainty (20%), as per Sebi’s findings—views largely unchanged since 2015.

Among non-investors, 34% cited fear of losing money as the key deterrent, followed by lack of knowledge on how to start investing and limited trust in products or financial institutions.

Sebi found that salaried individuals were more inclined to invest (23%) than the self-employed (17%), reflecting higher income predictability and comfort with structured savings.

Macro Factors Reinforcing Risk Aversion

Risk aversion isn’t just behavioral—it’s macroeconomic. Between 2011-12 and 2023-24, financial liabilities rose sharply from 12% to 26% of household savings. As more income goes toward loan repayments and fixed EMIs, investors prioritize capital protection and stable returns over riskier, high-yield opportunities.

In such an environment, “preservation of capital” naturally outweighs the pursuit of aggressive market gains.

The Way Forward: Bridging the Awareness–Action Gap

The Sebi survey underlines a familiar paradox in India’s financial landscape—high awareness, low participation. The next phase of financial inclusion must therefore focus on investor education, trust-building, and accessibility, not merely on product visibility.

Empowering individuals to move from awareness to action will require simplified communication, digital-first platforms with advisory integrity, and stronger investor-protection narratives.

For deeper insights into how investor education, behavioral finance, and risk-aware investing are shaping India’s wealth-management ecosystem, explore perspectives from Ranjit Jha (CEO)—a leader in bridging trust, research, and technology in wealth creation.

To learn how Rurash Financials empowers investors through structured advisory, AIF access, and digital wealth solutions, visit the official website.