Most investors run their SIPs in a straight line. A certain amount goes into equity, a certain amount into debt, and the pattern rarely changes. It is simple, it is convenient, and it avoids decision fatigue. This is what we have advocated all along and we still do. After all, investing in mutual funds is a hands-free approach, right?

However, its effectiveness doesn’t confine us from exploring strategies which are less conventional, slightly sophisticated and suitable for an advanced investor in search of ideas to beat fellow investors. And that’s why we looked at whether the RBI’s repo rate can be a strong macro-economic signal to derive an “SIP strategy”.

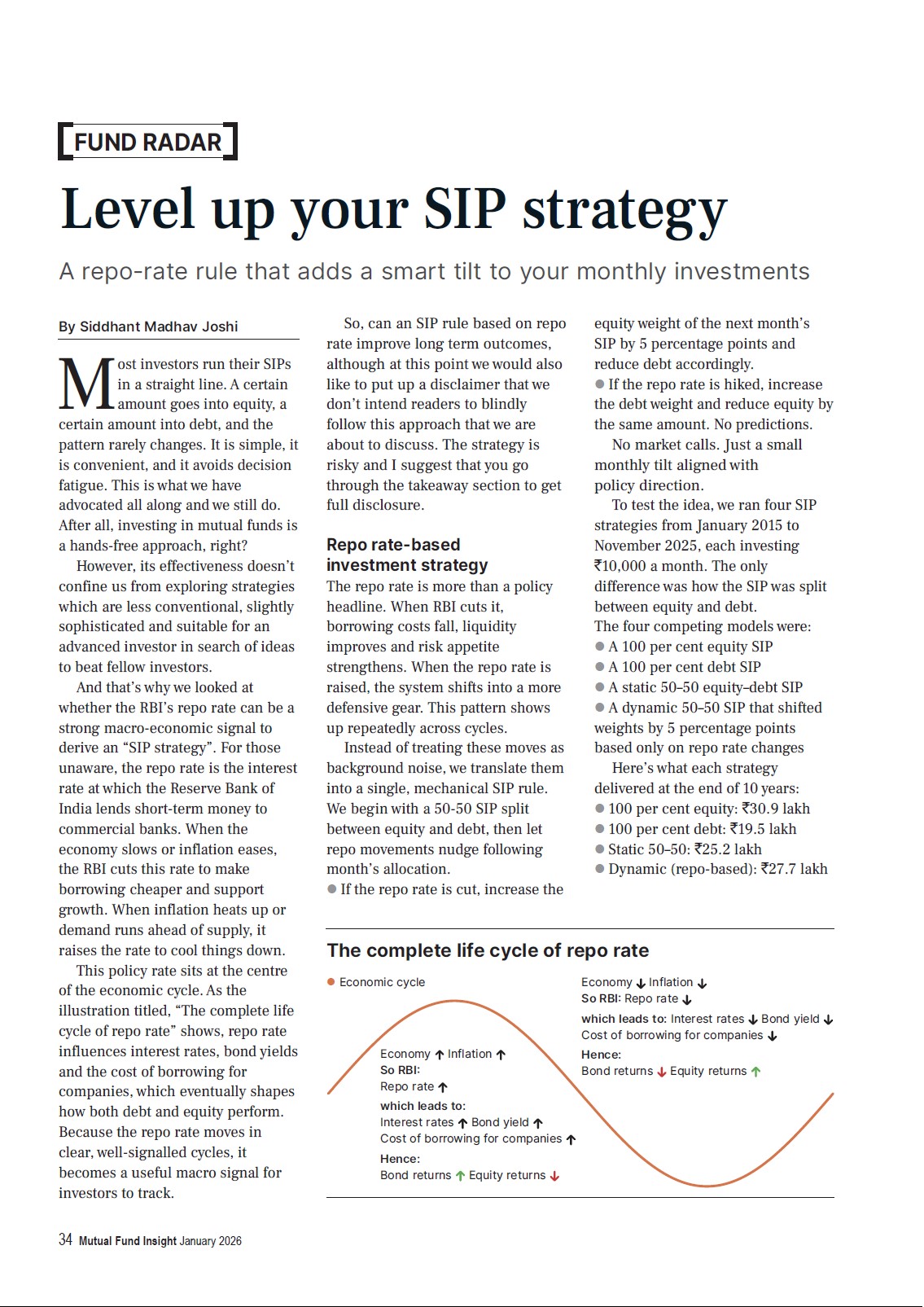

For those unaware, the repo rate is the interest rate at which the Reserve Bank of India lends short-term money to commercial banks. When the economy slows or inflation eases, the RBI cuts this rate to make borrowing cheaper and support growth. When inflation heats up or demand runs ahead of supply, it raises the rate to cool things down.

This policy rate sits at the centre of the economic cycle. As the illustration titled “The complete life cycle of repo rate” shows, the repo rate influences interest rates, bond yields, and the cost of borrowing for companies, which eventually shapes how both debt and equity perform. Because the repo rate moves in clear, well-signalled cycles, it becomes a useful macro signal for investors to track.

So, can an SIP rule based on repo rate improve long-term outcomes? At this point, we would also like to put up a disclaimer that we don’t intend readers to blindly follow this approach. The strategy is risky, and we strongly suggest going through the takeaway section to understand the full disclosure.

Repo rate-based investment strategy

The repo rate is more than a policy headline. When RBI cuts it, borrowing costs fall, liquidity improves and risk appetite strengthens. When the repo rate is raised, the system shifts into a more defensive gear. This pattern shows up repeatedly across cycles.

Instead of treating these moves as background noise, we translate them into a single, mechanical SIP rule.

We begin with a 50–50 SIP split between equity and debt, then let repo movements nudge the following month’s allocation.

If the repo rate is cut, increase the equity weight of the next month’s SIP by 5 percentage points and reduce debt accordingly.

If the repo rate is hiked, increase the debt weight and reduce equity by the same amount.

No predictions. No market calls. Just a small monthly tilt aligned with policy direction.

To test the idea, we ran four SIP strategies from January 2015 to November 2025, each investing ₹10,000 a month. The only difference was how the SIP was split between equity and debt.

The four competing models were:

100% equity SIP

100% debt SIP

Static 50–50 equity–debt SIP

Dynamic 50–50 SIP that shifted weights by 5 percentage points based only on repo rate changes

Here’s what each strategy delivered at the end of 10 years:

100% equity: ₹30.9 lakh

100% debt: ₹19.5 lakh

Static 50–50: ₹25.2 lakh

Dynamic (repo-based): ₹27.7 lakh

Equity, as expected, retains its position as the top performer over the long term. But the more meaningful comparison is between the two mixed portfolios. The dynamic repo-driven strategy ended significantly higher than the static 50–50 mix despite using the same total SIP amount and the same asset classes.

Why did this strategy work?

Rate cuts usually arrive when growth softens or when financial conditions tighten. These phases often coincide with weaker equity sentiment and more attractive valuations. By nudging more money into equity after each cut, the strategy puts fresh capital to work at favourable entry points.

Rate hikes surface when inflation builds or when the economy risks overheating. These are the moments when equity markets are more prone to volatility or shallow corrections. Redirecting a larger share of the SIP towards debt in those months improves portfolio stability and captures higher prevailing bond yields.

The real strength of this approach lies in its discipline and predefined rule-based structure. Allocation changes only by five percentage points at a time, avoiding behavioural traps such as going all-in or all-out based on noise. The SIP continues uninterrupted only the tilt changes.

Over a 10-year period, this small but steady alignment with policy cycles helped the dynamic portfolio participate better in recoveries and protect capital during tightening phases. The effect is subtle, but over long horizons, it is meaningful.

What investors should be aware of

The repo-based SIP strategy outperformed the static 50–50 mix in this specific 10-year window, suggesting that a macro indicator can act as a practical guide for allocation shifts.

However, this outcome must be interpreted with caution. The back-test reflects a unique decade shaped by liquidity cycles, policy responses, and economic shocks. Future market environments may not behave the same way.

Macro-economic indicators themselves are not constant.

Think of this strategy as a starting point, not a prescription. It simply demonstrates that even a single policy rate, when used systematically, can influence long-term SIP outcomes. Turning it into a live framework requires customisation, risk awareness, and discipline to stay the course.